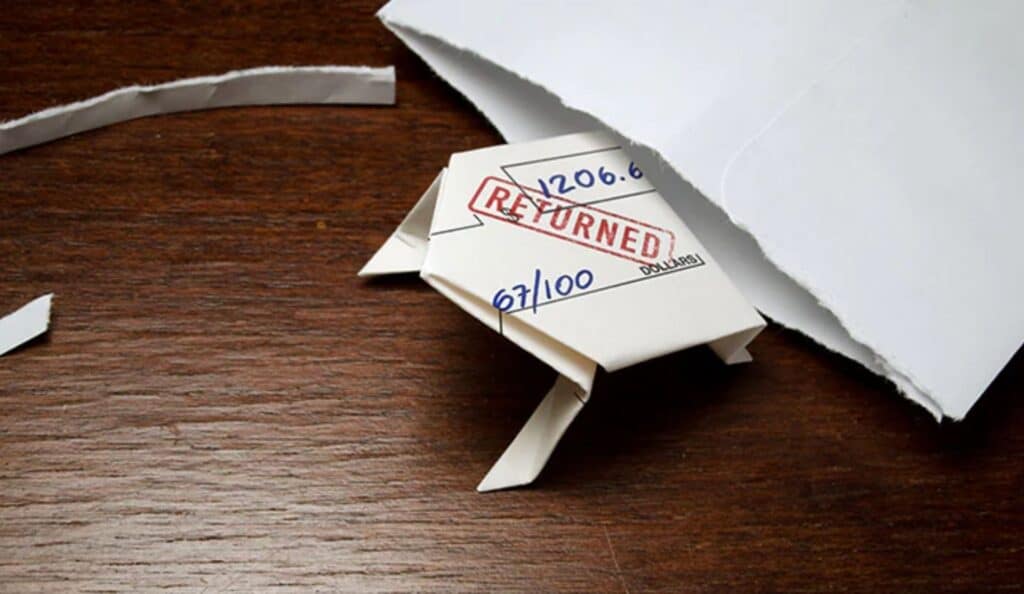

A returned check fee is a penalty a bank charges when a check you write or receive cannot be processed because your funds aren’t sufficient, either your account is closed or there are other issues.

However, it is possible to add additional charges and impact your finances and if you are a business owner who accepts checks or a person who writes them it’s essential to understand how these fees work. Moreover, these charges will vary, from bank to bank, and knowing how the fees are structured is crucial.

What is the Returned Check Fee?

A returned check charge also known as an NSF charge is a bank charge for bad checks. It is intended to discourage individuals from issuing checks when they don’t have sufficient funds. Typically, the individual who issued the check pays the fee.

However, the recipient of a bounced check may experience issues if they attempt to deposit it. If the check is returned, the funds will not be credited to their account, and they may have a negative balance, which can result in overdraft fees, and moreover, if the issue is not resolved within 30 days, it can damage their credit score. If the payment is not collected, the lender can raise interest rates, employ a collection agency, or sue the borrower, which can also damage the credit score.

Creditors also compel individuals to pay various fees, such as service fees, minimum balance fees, and debit transfer fees. There are also other fees for services such as bounced checks, late payments, and declined payments. They usually range between $25 and $40 and may occur if there is insufficient cash in the account, the account is closed down, or there is an issue with payments.

They are typical with checks but may also occur with online or automatic payments. Individuals need to be cautious when they issue checks or make automatic payments because they may not have sufficient cash on the day they are issuing payments.

Late fees and interest can be charged, but there will not be other fees like returned payment fees and bounced check fees. However, the individual can simply discontinue automatic payments or change to an account with enough money to avoid a returned payment fee. Moreover, creditors are required to include the fees in the contract.

What are the Consequences of a Returned Check?

The consequences of writing a bad check when you are not financially stable can be very detrimental. You may face a fee from your bank, have difficulty with stores and providers of services, and get your bank account closed if it happens frequently.

Penalties in Financial Field

When you write a check that doesn’t have sufficient funds, you could be charged additional fees, based on the bank. A bounced check typically incurs a fee of roughly $25. It can also lead to issues for some businesses. Though these incidents don’t typically appear on credit reports immediately, they can damage your credit score over the longer term. Your bank may report you to a credit agency, or your debt might be sent to a collection agency, which can harm your credit score.

Impact on Credit Card and Score

If banks might not be able to collect their money back after checks bounce, that could affect your credit score. Each time a debt goes to a collection agency, it can be reported to credit agencies for seven years or so. If you continue to accrue overdrafts, your bank may have to close your account, which can also have an effect on your credit score if reported.

Impact on Legal Issues

Just like passing a fake check is a fraudulent crime, passing bad checks can also get you in legal trouble, including misdemeanors or felonies in some areas. However, consumers have certain rights that shield them from predatory collection practices, give them the option to dispute errors, and allow them to seek legal help. It is critical for people to understand their rights and the financial stakes.

How Much Does The Returned Fee Cost?

If a check bounces, the fee can be between $10 and $40, depending on the bank. Different banks have different fees for bounced checks. For example, U.S. Bank charges $19, PNC Bank charges $36, Chase charges $34, Truist has no charge, and Bank of America charges $35. Overdraft protection is an extra cost that lets the bank pay the check even if there isn’t enough money in the account.

Without overdraft protection, the bank may not pay the check and will charge a non-sufficient funds (NSF) fee. This fee is like a returned item fee and can be charged every time the bank tries to process a check or transaction without enough money. If someone writes a bad check for $300 but only has $250 in their account, there will be fees.

Overdraft protection can also lead to an overdraft fee, which can be up to $35. In 2021, big banks like Wells Fargo and Bank of America made over $1 billion from overdraft fees. For smaller banks, overdraft fees made up to a third of their income.

If the person who wrote the check doesn’t have overdraft protection, they will keep the $250 in their account and be charged an NSF fee, which is about $34. Writing a bad check can cost between $35 and almost $70.

Because of new rules, many big banks have stopped charging overdraft fees, which may help reduce late payments. Telling customers about the risks of bouncing a check can help them avoid late payments.

Some Causes of Returned Check

Information Regarding Incorrect Account

Incorrect account information, such as mistakes or outdated information, can lead to returned payment charges. The mistakes can lead to transactions that are declined and can happen because of bank errors. Incorrect account information can lead to unnecessary fees on bounced checks.

Overdraft Limits of Accounts

Going over your account’s overdraft limit will cost fees and financial strain. It is wise to prevent these issues by choosing an overdraft protection plan that has low interest and fees and checking your balance. Having a balance in your account will avoid overdrafts. If you have multiple accounts, have enough money in the right account before you send money to avoid delays and charges.

Low Funds of Account

Low funds in your account can also lead to returned payment charges. To avoid this, monitor your account activity on a regular basis and ensure that you have sufficient funds for your transactions. Automatic payments or low-balance reminders may assist you in managing your funds.

Overdraft Protection

Overdraft protection could have extra fees, so balance the benefits and costs before you choose it. Keep track of payment due dates and pay bills in a timely manner to avoid late fees and harm to your credit record. You need quick and accurate information for your bank account to operate.

Ways to Avoid and Prevent Returned Check Fees

Getting customers to pay automatically avoids bad checks and additional fees. Internet payments are simpler and less expensive to receive than checks. Certain services have the ability to verify how much money one has before accepting their check, which prevents bad checks. Simple payment guidelines can prevent customers from writing insufficient funds checks, and lowering fees and bad checks.

Companies can establish overdraft protection with their bank to prevent bounced checks. To ensure you have sufficient funds prior to writing a check, monitor your account balance, establish overdraft notices, monitor your transactions correctly, receive direct deposit of your paycheck, connect your checking account to an overdraft savings account for assistance, and check your credit report regularly for errors. Direct deposits assist in getting money into your account on time, without problems of insufficient funds. To prevent check return fees, the best option is to ensure there is sufficient money in your account before writing a check. It is however advisable to regularly check your balance and monitoring transactions can prevent overdrafts. Another option to prevent fees is to arrange overdraft protection, which enables the bank to cover any deficits, but it can have its own fees.

Moreover, check return fees can add up fast, particularly if there are a number of bounced checks. Bounced checks may also damage your credit rating, and it becomes more difficult to obtain credit in the future. In order to steer clear of these charges, become familiar with your bank’s policies and fees on returned checks, which you can typically locate in your account terms or by contacting a bank representative.

Subsequently, if a check is returned due to a bank error, you may be able to waive the fee with documentation of the error. Keep in mind, that check return fees are only one kind of bank fee; there are ATM fees, monthly account fees, and additional overdraft fees. Shopping around and selecting the appropriate account can save you from these fees.

Steps To Take If It Was a Bad Written Check

Contacting the Receiver in Time

If you’ve written a bad check unintentionally, and you catch it in time, you can steer clear of trouble in several ways. The only thing to do, first, is have a conversation with the person who received your check so that they won’t cash it. If they haven’t cashed it yet, ask whether you can pay them in another manner or postpone the payment. This will maintain your cordial relationship with them.

Visiting the Bank

You can also stop the check by your bank’s website, through an app, or by calling or visiting the bank. Provide them information such as the check number, the amount, to whom it was made out to, and when you wrote it. Your bank may impose a fee for this, but it’s generally a small price to pay to avoid much larger headaches.

A Lesson to Learn

Lastly, view bounced checks as a lesson to learn from. If you do need to pay a fee, work on your money habits to prevent this in the future. You can use your own bank’s app or budgeting tools to help you stay on top of what’s in your account so you don’t get blindsided by large checks.

Conclusion

To avoid problems and extra costs from bounced checks, it’s important to have good banking habits. Keep an eye on your account balance, set up overdraft protection, and use automatic payments to prevent bounced checks.

Knowing your bank’s fees and rules can help you avoid extra charges. If you write a bad check, contact the person or your bank right away to fix the issue. In the end, managing your money well and staying aware of your finances will help you avoid bounced check fees and keep your finances in good shape.